Where to start

How We Estimate the Costs of Systemic Inefficiency and Corruption

The important thing to keep in mind about corruption is that it is everywhere and in every government.

The risk of funds being used for some other purpose than for what it was intended is always higher than zero. Where there is data, we can quantify risks and measure costs. When it comes to putting a dollar figure on corruption for a country or a sector, it is complicated and sensitive.

It is very hard to get agreement on a consistent methodology and therefore easy for vested interests to undermine efforts to try. Politically, corruption is very sensitive as it can undermine the confidence of the public in their governments. It is why autocratic models of government and corruption often go together. This makes it hard to have an honest and open discussion about the true costs of inefficiency and corruption.

AFI directors spent years in Afghanistan trying to raise these issues internally, with government officials and donor partners putting billions of dollars into governance. To no avail, there was little appetite to challenge powerful vested interests who were stealing the money. Everyone accepted that corruption was bad, but with no specific way to measure the cost, no serious change was possible. We believe this significantly contributed to the eventual outcome.

We have concluded that developing a robust and consistent approach to costing inefficiency and corruption and making it public is a necessary step towards a more constructive discussion about what needs to be done.

In 2020, we published a paper on something we call the “Follow-the-Money Corruption Cycle: Revealing National Accountability Failures”[1]. It was very frank about how corruption can work in any public finance system.

It showed how the very systems that are designed to control corruption and promote government efficiency can end up facilitating corruption.

In the extreme, public finance systems can be used as the foundation for formidable cultures of corruption within the very institutions entrusted by the public to help deliver good governance.

By being clear on where and how corruption works in the public finance system we believe that corruption can be better targeted where it matters most to strengthen public accountability and improve government efficiency and effectiveness.

The figure below provides an overview of the “follow the money corruption cycle”.

[1] See How Corruption Works in the Public Sector—One Easy Lesson (imf.org)

Focus First on the

Follow-The-Money Corruption Cycle

The Underbelley

of Public Finance Systems

The “follow-money corruption cycle” shows how all parts of the budget cycle work and where the risks are for corrupt activities. The scale of the problem becomes clearer as each corruption risk point is highlighted throughout the cycle. To keep things simple the following describes the basic corrupt objective at each one of the eleven (11) points of the “follow-money corruption cycle”.

The model uses a risk-based approach to quantify the costs of corruption and efficiency losses caused by weak public finance systems. The methodology adopted is the same we have used in various Fiduciary Risk Assessments (FRAs) but is adapted to enable assessment of risks and losses at all points in the “follow-the-money corruption cycle”. The methodology also builds on methodologies used elsewhere including on estimating costs of corruption in procurement.

Being Frank About How Corruption Can Work

Within Public Finance Systems

- Starting at the budget you pay to get your budget or your preferred policy, including under an auction like arrangement, rather than having the budget allocate resources based on well developed policy and strong evidence[1].

- At the commitment phase you pay to get access to the allotment (or approval to spend the budget), rather than using the commitment system to manage cash and ensure appropriations (legal authorities) are not breached.

- At the procurement stage you pay to win contracts, rather than using it to support competition to keep costs down and quality up.

- At the contract management stage you pay to change contracts to make them more profitable, rather than ensure contract terms are complied with.

- At the verification and payment stage you pay to falsely verify that goods and services were delivered on time and to specification, and then pay again to get paid, rather than ensuring payments are made in accordance with contracts.

- At the audit stage you pay for audit irregularities to be cleared, whether those irregularities are real or otherwise (i.e., made-up to get more bribes or to punish), rather than audit providing assurances that financial information is accurate and believable and auditing being a reliable mechanism to support institutional learning.

- At the personnel and payroll stage you pay for positions and pay to retain positions through family connections or outright bribes or cashing in old debts and favours, rather than promoting merit-based recruitment and retention.

- At the accounting stage you pay to facilitate licit and illicit movements of funds through the accounting systems and to cover tracks, rather than ensuring accounting, classification and reporting rules are followed.

- At the revenue collection stage you pay to facilitate favourable treatments of what you owe or what you are paying for (including for illegitimate/illegal goods or services) or speed up intentional or unintentional slow administrative processing, including in service delivery areas, rather than ensuring revenue is assessed and collected in accordance with the rules.

- During balance sheet management phases you pay to secure favourable treatments of assets and liabilities – e.g. have debts written off and acquire assets cheaply, rather than ensuring assets and debts are managed well.

- If then, at any point in the cycle evidence of malfeasance emerges and results in referrals to any or all the accountability institutions (like the police, anticorruption commission, prosecutors, inspector generals, and auditors) you just pay again to clear the allegation, investigation, prosecution, finding or sentence, rather than ensuring checks and balances are working as intended and the rule of law is respected.

In a country with systemic corruption throughout the “follow the money corruption cycle”, it can clearly be seen that there is very little public money left to finance good quality fiscal policy aimed at improving the efficiency and effectiveness of core public services like health, education, public works and defence.

The approach takes the “follow the money corruption cycle” structure of public finance sub-systems to provide clarity of where and how corruption works in government systems and ultimately to estimate the costs of corruption and efficiency losses at the sub-system level.

[1] See also Laing, 2017, “The Blight of Auction-Based Budgeting: What is it and how can we deal with it?” http://effectivestates.org/wp-content/uploads/2017/09/Auction-Based-Budgeting-WEB.pdtf

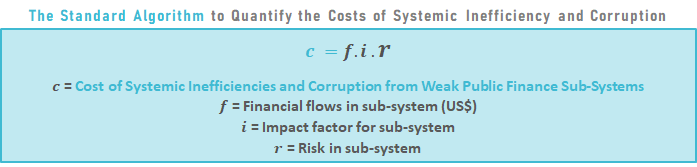

A simplified version of the formula used to quantify financial impact of weak PFM systems … or in other words … the costs of corruption and inefficiency is above. There are three parameters used in the costing algorithm:

- Quantified development or fiduciary risks (r) representing a good enough proxy for likelihood of risks materialising, including inefficiency and leakage (the current model uses development risk);

- Impact factor (i) is based on assessed importance of the public finance sub-system to efficiency and leakages; and

- Financial flows through the financial sub-system (f). The financial flows and pecuniary significance rates for every country were drawn from Government Finance Statistic (GFS) data on components of fiscal flows and stocks for every country. Likelihood (or risk) multiplied by impact factor multiplied by financial flows in the sub-system gives an approximate financial estimate for inefficiencies and corruption in the sub-system. The formula is effectively a simple linear equation where r and i form the slope parameter with variables f and c.

the Three Steps to Estimate the Losses

Step 1

Quantify Risk

Quantify risk of inefficiency, corruption, and system weakness – We use a modified index of indexes approach for Development Risk – the risk of not achieving development goals due to weak public finance systems. Our methodology is here.

Step 2

Apply Impact Factors

Apply impact factors for the relevant part of the public finance system. These are drawn from field work and confidential interviews

Step 3

Measure Amount of Funds Flowing through the Systems

Use GFS Data and economic classification categories for fund flows then apply costing algorithm

The results can be shown in various ways. The most simple way is just to report the losses in terms of dollar value. These can be in nominal or real terms (i.e. adjusting for the effects of inflation). To be able to compare losses between countries, the dollar value is not that helpful as it doesn’t account for differences in size of the country or economy. Other ways to show losses include representing the dollar value of losses as percent of: i) total government expenditure; ii) total government revenue; and iii) of GDP, or it can be shown on per capita terms. While there is plenty of fiscal and risk data to calculate losses, standard annual results would normally be limited to having sufficient risk and fiscal data available in the same year. Consequently, period averages are used to deal with this problem. The annual and period average results can be shown in league tables that rank countries.

The Costs of Inefficiency and Systemic Corruption (COSIC) Index is the first version of such a legal table. AFI are currently piloting it to assess its usefulness to reformers and other stakeholders. An interactive version of the COSIC Index is provided below. Users can choose how to rank countries by the different loss measures (by clicking on the relevant heading), and can also drill down on certain groups of countries and years and can also chose what level of government to draw the fiscal data from. There are different views that can be scrolled through (using the arrow buttons at the bottom). The first view is the standard league table of 6 different measures of losses plus the average development risk for the country and period. The second provides four frequency distribution charts of development risk, showing distribution by income status, region, year and fragility. The third provides heat tables of the seven measures summarised by income group, region and fragility. The fourth is an alternative layout of the first.